MAY 3, 2021

LIBIN ZHANG

Libin Zhang is a partner at Fried, Frank, Harris, Shriver & Jacobson LLP in New York.

In this special report, Zhang examines, using charts and figures for both readers and visual learners, the potential outcomes under President Biden's current and future proposed tax increases for individuals and corporations. He also explains how those increases could affect New York City taxpayers in particular.

Copyright 2021 Libin Zhang.

All rights reserved.

The Tax Cuts and Jobs Act — the 2017 tax reform and simplification law — reduced individual and corporate federal income tax rates. President Biden has proposed to increase those rates. Corporate tax increases have been proposed to pay for a $2 trillion infrastructure plan,1 while individual tax increases are anticipated to pay for other spending programs.2

If those tax increases take effect, New York City resident individuals may be subject to combined federal, state, and local marginal income tax rates of over 65 percent, while corporations and their shareholders subject to New York City taxes may have a combined marginal tax rate of over 75 percent. Some decedents’ estates would pay marginal income and estate taxes that add up to over 80 percent. The higher tax rates could encourage migration to lower-tax states, expatriations to lower-tax countries, greater personal consumption spending by the wealthy and elderly, and other taxpayer responses.

This article focuses on the highest statutory marginal income tax rates and does not address phaseouts of tax benefits that may result in even higher marginal tax rates, including the approximately 65 percent marginal federal income tax rate for individuals subject to the section 199A passthrough business income deduction phaseouts.3 This article also does not focus on other contemplated tax reforms such as Treasury’s proposal for stopping harmful inversions and ending low-tax developments (SHIELD)4 and possible future initiatives that may include Stopping Worldwide Offshoring and Related Developments (SWORD), Bringing Uniformity to Complex and Kaleidoscopic Large Entity Returns (BUCKLER), Harmonizing Asset Mobility and Movement Enforcement and Repatriation (HAMMER), and High-Yield Discount Redemption Adjustment (HYDRA).

The TCJA reduced the individual federal income tax rate from 39.6 percent to 37 percent for 2018 through 2025. Partially in exchange, the TCJA generally capped an individual’s or married couple’s annual deduction of state and local income and property taxes for 2018 through 2025 at $10,000.5

During his presidential campaign, Biden proposed restoring the highest federal income tax rate back to 39.6 percent, which may be retroactive to January 1, 2021. A historical precedent is the Revenue Reconciliation Act of 1993 (P.L. 103-66), which President Clinton signed into law on August 10, 1993, after it received a 219-213 vote in the House and a 51-50 vote in the Senate (Vice President Al Gore broke the tie). The law increased the highest marginal individual federal income tax rate as of January 1, 1993, from 31 percent to 39.6 percent.

Although Congress enacted the American Rescue Plan Act of 2021 (P.L. 117-2) in February as a budget reconciliation bill with 50 Senate votes in favor, Congress can enact a second reconciliation bill later in 2021 that could raise taxes without being subject to a Senate filibuster. Reconciliation bills are generally allowed once per fiscal year that begins on October 1, and the Senate’s parliamentarian has further clarified that Congress may pass multiple reconciliation bills in a single fiscal year by editing the same underlying budget resolution.6

It is unclear whether Biden will restore the ability to fully deduct state and local taxes. An unlimited deduction would disproportionately benefit higher-income taxpayers who pay the most state and local taxes. Democratic lawmakers from high-tax states have been pushing for a repeal of the SALT deduction cap,7 but a restoration of the deduction to help higher-income taxpayers in high-tax states was not mentioned in the Biden-Sanders Unity Task Force Recommendations.8

A SALT deduction cap repeal may encourage state and local governments to increase their income tax rates. In a possible example of comparing unhatched chickens and oranges, New York Gov. Andrew Cuomo (D) explained on April 7 that the state’s recently proposed income tax increases of around 2 percent are justifiable as they “anticipate a SALT repeal” and would really result in a “net reduction in taxes.”9 The New York legislation appears to be missing language that would make the tax increase contingent on SALT cap repeal. Even a full SALT cap repeal may not be useful for higher-income taxpayers who would pay the alternative minimum tax and cannot claim any SALT deduction for AMT purposes.

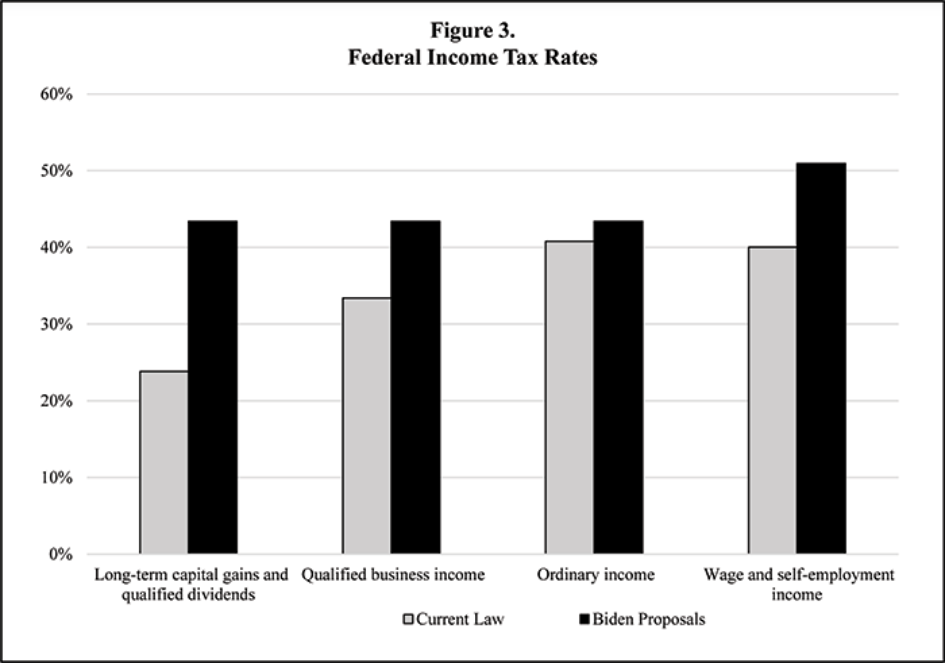

When combined with the 3.8 percent section 1411 Medicare tax on net investment income, the marginal individual federal ordinary income tax rate would increase from 40.8 percent to 43.4 percent under the Biden tax proposals.

|

Ordinary Income |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

37% |

39.6% |

|

Section 1411 net investment income tax |

3.8% |

3.8% |

|

Total marginal ordinary income tax rate |

40.8% |

43.4% |

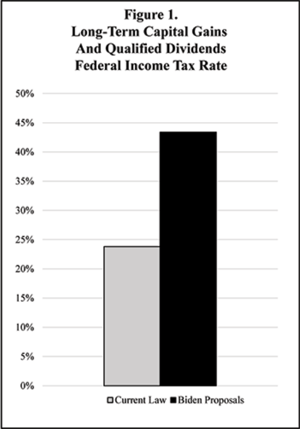

One of Biden’s more widely discussed proposals is to increase the individual federal tax rate for long-term capital gains and qualified dividend income to 39.6 percent for taxpayers with more than $1 million of income. Income is not defined but is presumably adjusted gross income of a single individual or married couple, and adding back foreign earned income exclusions.

It was originally not apparent whether that 39.6 percent top rate includes the 3.8 percent section 1411 tax. On the assumption that the intent is to equalize the federal tax rates for ordinary income, long-term capital gains, and qualified dividends, the marginal individual federal tax rate for the latter two income types would almost double from 23.8 percent to 43.4 percent.

|

Long-Term Capital Gains and Qualified Dividends |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

20% |

39.6% |

|

Section 1411 net investment income tax |

3.8% |

3.8% |

|

Total marginal long-term capital gains and qualified dividends tax rate |

23.8% |

43.4% |

A higher federal income tax rate for long-term capital gains would encourage investments into assets that generate tax-free types of capital gain, such as those from the sales of principal residences,10 section 1202 small business stock, and some qualified opportunity fund investments held for at least ten years.11

The TCJA enacted section 1061, which generally imposes — on some carried interests and other partnership profits interests — a three-year holding period instead of a one-year holding period to qualify for the long-term capital gains rate. Although Biden and other Democrats have discussed additional carried interest legislation in the past, it is possible that the general increase in long-term capital gains rates would subsume and eliminate the need for more specific carried interest legislation. Section 1061 would continue to be relevant for mom and pop private equity managers who make less than $1 million a year.

On the other hand, some Democratic members of Congress have proposed legislation in early 2021 to treat carried interest gains and dividends as ordinary income that is subject to self-employment taxes.12 The bill would generally disallow the zero percent tax rate for section 1202 small business stock gain that is allocated to carried interest.

The potential enactment of carried interest legislation may lead to a variety of reactions, including sales of portfolio companies and carried interest stakes in late 2021 before new legislation takes effect. However, the Carried Interest Fairness Act of 2021 is proposed to be effective for tax years ending on or after its enactment date, which may retroactively cover carried interest income realized since January 1, 2021.

The TCJA decreased the federal corporate income tax rate from 35 percent to 21 percent starting in 2018.13 To loosely equalize the post-TCJA federal income tax burdens for corporate businesses and noncorporate businesses, the TCJA enacted the section 199A passthrough business income deduction for 2018 through 2025. The deduction generally reduces the federal tax rate by 20 percent for some business income, ordinary real estate investment trust dividends, and ordinary income from some publicly traded partnerships. The deduction is unavailable for higher-income investors in publicly traded partnerships and other businesses that engage in some personal services and financial activities.

Biden has proposed to eliminate the section 199A passthrough business income deduction for higher-income taxpayers. Like most of his individual tax proposals, the elimination would apply only to taxpayers who make more than $400,000 a year. There has been confusion over whether the $400,000 threshold is for married couples or individuals. White House Press Secretary Jen Psaki said on March 17 that the $400,000 threshold is only for families,14 but she clarified on March 24 and March 29 that the $400,000 threshold is per individual.15 Either way, the change would cause qualified business income, ordinary REIT dividends, and some PTP income to be taxed at the same marginal federal rates as other ordinary income.

|

Qualified Business Income |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

37% |

39.6% |

|

Section 199A passthrough business income deduction |

-7.4% |

0% |

|

Section 1411 net investment income tax |

3.8% |

3.8% |

|

Total marginal qualified business income tax rate |

33.4% |

43.4% |

Biden has raised the prospect of restricting real estate losses, which may involve reforming the section 469(c)(7) real estate professional rules and changing bonus depreciation and depreciation recovery periods for real property. For instance, included in the Consolidated Appropriations Act of 2021, which was passed nearly unanimously, is 100 percent bonus depreciation for the seven-year property that is any motorsport entertainment complex placed in service from 2021 through 2025,16 which helps address any shortage of NASCAR racetracks during and after the COVID-19 pandemic.

Given the potential increase in income tax rates, individuals may consider increasing their taxable income and locking in the lower tax rates while they are still available. For example, taxpayers can accept prepayments of rents and service income, defer depreciation and other deductions, and realize more taxable gains in sales and wash sales. Charitable contributions can be postponed until the taxpayer gets better bang for the donated buck, stock, or conservation easement. Taxpayers who are trying to win the lottery should try to win earlier and select the lump sum. Those with qualified opportunity fund investments can consider several common ways to trigger their deferred eligible capital gains earlier than December 31, 2026, while still preserving the ability to sell their qualified opportunity fund investment free of federal income tax after ten years.17 Other taxpayers might consider renouncing their American citizenship when they can avoid or minimize their section 877A expatriation tax, or they can make a bona fide move to Puerto Rico and avoid U.S. federal income taxes on their income from Puerto Rico sources.18

Currently the 12.4 percent Social Security tax and the 12.4 percent non-Medicare portion of the self-employment tax do not apply to wages and self-employment income over the Social Security wage base ($142,800 in 2021). The Social Security tax is nominally half paid by the employer and half paid by the employee.19 Wages and income over the wage base are subject to only the Medicare tax or the Medicare portion of the self-employment tax, which is either 2.9 percent or 3.8 percent.20

Biden has proposed to impose the 12.4 percent payroll taxes on wages and self-employment income over $400,000. The “donut hole” effect, known in some circles as the “bagel hole” effect, is that the 12.4 percent payroll taxes would be avoided only for income between $142,800 and $400,000, but would apply to income above and below that range. Similar legislation was introduced on January 30, 2019, in the well-known Social Security 2100 Act (H.R. 860), which had over 200 cosponsors in the House and would have also increased the payroll taxes from 12.4 percent to 14.8 percent.

The self-employment tax totals 15.3 percent when both the 3.8 percent Medicare portion and the 12.4 percent non-Medicare portion are counted. Some commentators have added the 15.3 percent self-employment tax to the 39.6 percent federal income tax to arrive at a marginal federal income tax rate of 55 percent. However, the self-employment tax burden is slightly less because it is imposed on only 92.35 percent of self-employment income and is half deductible for federal income tax purposes.21 The combined marginal federal income tax burden on self-employment income is therefore around 51 percent.

|

Self-Employment Income (assume no 199A deduction) |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

37% |

39.6% |

|

Self-employment tax (on 92.35% of income) |

2.7% |

14.1% |

|

Federal deduction for half of self-employment tax |

-0.5% |

-2.8% |

|

Additional self-employment Medicare tax (on 92.35% of income) |

0.8% |

0.8% |

|

Total marginal self-employment income tax rate |

40% |

50.9% |

A somewhat different computation would usually arrive at the same combined federal income tax rates for wage income, after counting both employer and employee halves of the Social Security tax.

When President Franklin Delano Roosevelt signed the Social Security Act of 1935, which created a 1 percent payroll tax on the first $3,000 of income, Social Security was designed as a contribution system so that an individual’s retirement benefits were generally based on how much they contributed to the system. Every individual receives an annual Social Security statement noting how much they have paid in payroll taxes and how much they should expect as retirement benefits that are generally proportional to those payroll tax payments. The expansion of Social Security contributions to cover significantly higher incomes would presumably mean that the corresponding Social Security payments to those retirees would be significantly increased as well.

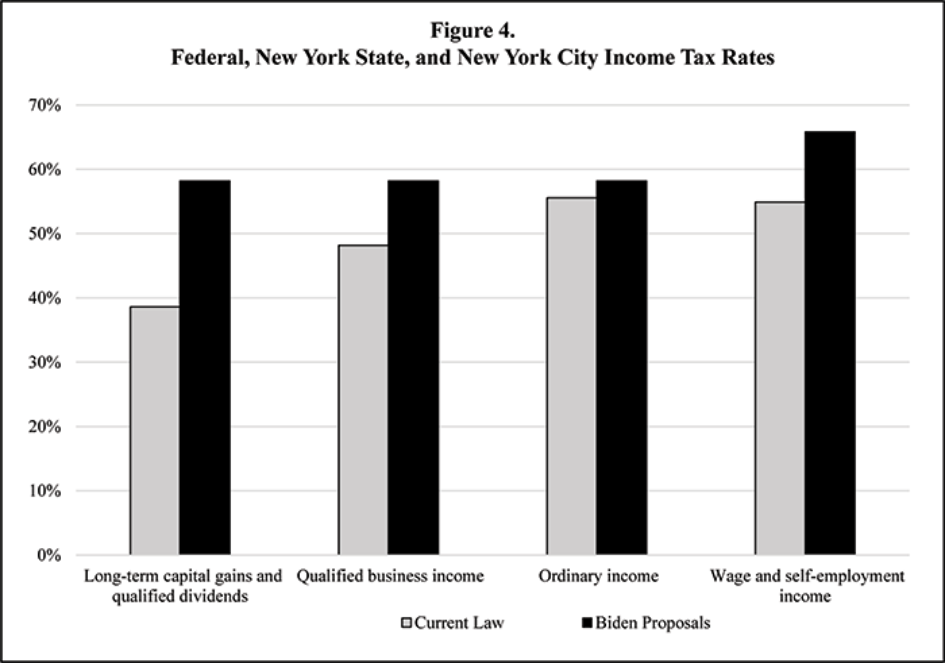

Most parts of the United States are subject to state income taxes and sometimes local income taxes. For example, a New York City resident is subject to the city personal income tax of up to 3.876 percent and the state personal income tax of up to 10.9 percent under recently enacted New York budget legislation that is retroactive to January 1, 2021, and effective through 2027.

Assuming that the state and local taxes are not fully deductible for higher-income taxpayers, a New York City resident’s combined income tax rates for ordinary income, long-term capital gain and qualified dividends, and qualified business income are shown in tables 5 through 8.

New York imposes the metropolitan commuter transportation mobility tax on self-employment income and wages in New York City and nearby counties. When all the taxes are added together and adjusted for various deductions, the city resident may be taxed at around 66 percent on self-employment income and wages.

|

Ordinary Income |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

37% |

39.6% |

|

Section 1411 net investment income tax |

3.8% |

3.8% |

|

New York state personal income tax |

10.9% |

10.9% |

|

New York City personal income tax |

3.9% |

3.9% |

|

Total marginal ordinary income tax (New York City resident) |

55.6% |

58.2% |

|

Long-Term Capital Gains and Qualified Dividends |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

20% |

39.6% |

|

Section 1411 net investment income tax |

3.8% |

3.8% |

|

New York state personal income tax |

10.9% |

10.9% |

|

New York City personal income tax |

3.9% |

3.9% |

|

Total marginal long-term capital gains and qualified dividends tax |

38.6% |

58.2% |

|

Qualified Business Income |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

37% |

39.6% |

|

Section 199A passthrough business income deduction |

-7.4% |

0% |

|

Section 1411 net investment income tax |

3.8% |

3.8% |

|

New York state personal income tax |

10.9% |

10.9% |

|

New York City personal income tax |

3.9% |

3.9% |

|

Total marginal qualified business income tax |

48.2% |

58.2% |

|

Self-Employment Income (assume no 199A deduction) |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal income tax |

37% |

39.6% |

|

Self-employment tax (on 92.35% of income) |

2.7% |

14.1% |

|

Federal deduction for half of self-employment tax |

-0.5% |

-2.8% |

|

Additional self-employment Medicare tax (on 92.35% of income) |

0.8% |

0.8% |

|

New York state personal income tax |

10.9% |

10.9% |

|

New York City personal income tax |

3.9% |

3.9% |

|

New York state and New York City deduction for half of self-employment tax |

-0.2% |

-1% |

|

Metropolitan commuter transportation mobility tax |

0.3% |

0.3% |

|

Total marginal self-employment income tax |

54.9% |

65.8% |

Also, self-employment income may be subject to the 4 percent New York City unincorporated business tax, which depends on the income sources at the unincorporated business level.

Other states may have similar marginal tax rate results for their residents. California has a top marginal state income tax rate of 13.3 percent, which may be increased to 16.8 percent to catch up with New York City. California legislators are also looking into imposing a wealth tax on individuals who have lived in the state for 60 or more days in any year during the previous 10 years.22

The increased tax burdens may encourage taxpayers to move to lower-tax states and localities. However, many taxpayers would continue to be subject to tax by high-tax states because of the sourcing of their income. A law firm partner who lives in Texas or Florida, for example, would be subject to Illinois income tax for Illinois-source income because of services performed in Illinois by any other law firm partners and employees. In contrast, an employee of the same firm who lives in Texas or Florida would not have any wage income sourced to Illinois. A law firm associate in a low-tax state who is promoted to non-equity partner of a national law firm with sizable Illinois, California, and New York offices may need to weigh the trade-off between (i) higher state tax liabilities because of source-state taxation of the guaranteed payments, the loss of many employee-specific tax benefits, and more complex state filings and (ii) the prestige of being a non-equity partner.

Biden has proposed to eliminate the section 1014 basis step-up at death. The plan is for death to be a realization event with a full federal income tax imposed on a decedent’s unrealized appreciation in his or her assets.23

Several proposed bills shed more detailed light on the step-up repeal proposal.24 The deemed realization would apply to both gifts and deaths, other than for transfers to a spouse or a charitable organization. An annual gain exclusion of $100,000 would apply to gifts, while the deemed realization at death has a $1 million exclusion. The $1 million exclusion for unrealized gains at death is more generous than a similar Obama administration proposal, which would have allowed an exemption of $100,000 per decedent.25

Biden has also proposed to increase the federal estate tax from 40 percent to 45 percent and reduce the federal gift and estate tax exemption, potentially down to the $3.5 million exemption amount that existed in 2009, without any adjustment for inflation. Currently, the exemption amount is $10 million through 2025 and $5 million thereafter, indexed for inflation from 2011.

States can impose their own estate taxes, such as 16 percent in New York and many other states. The combined estate tax burden for a New York decedent is shown in Table 9.

|

Estate Taxes |

Current Law |

Biden Proposals |

|---|---|---|

|

Federal estate tax |

40% |

45% |

|

New York estate tax |

16% |

16% |

|

Federal deduction for New York estate tax |

-6.4% |

-7.2% |

|

Combined estate taxes |

49.6% |

53.8% |

The estate tax and the income tax are not imposed on the same amounts, as the former is generally applied to the net value of the assets while the latter is imposed on the unrealized gain in the assets. A decedent may sometimes have unrealized gains over the net value of her assets, particularly if she owns leveraged properties or partnership interests with a negative tax capital account because of prior loss allocations and section 731 tax-free distributions. It is unclear how the federal government would collect taxes from an estate with insufficient net assets due to debt.

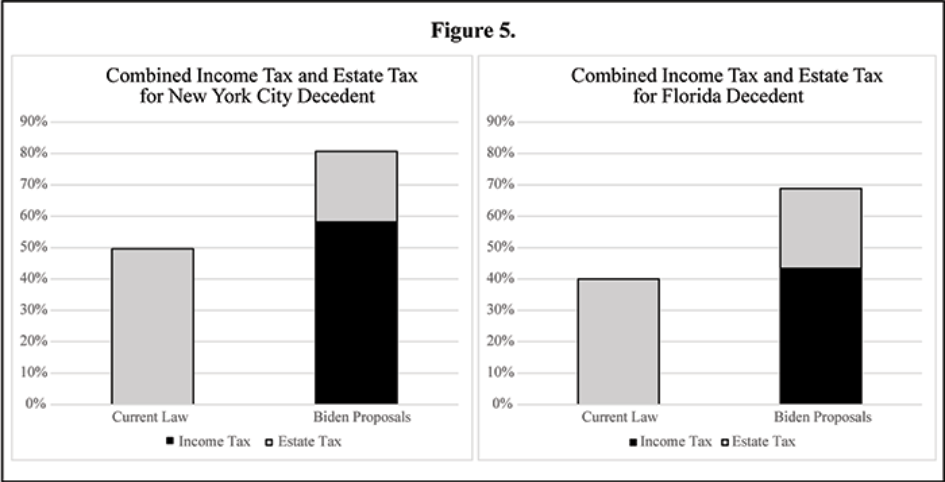

On the simple assumption that the income taxes and estate taxes are imposed on the same item, which is true for marginal amounts of unrealized appreciation in assets, the combined marginal income tax and estate tax burden for a New York City decedent is over 80 percent.

|

Income and Estate Taxes (New York City decedent) |

Current Law |

Biden Proposals |

|---|---|---|

|

Combined income tax |

0% (basis step-up) |

58.2% |

|

Combined estate tax |

49.6% |

53.8% |

|

Adjustment for reduced estate value because of income tax |

0% |

-31.3% |

|

Combined marginal income and estate taxes |

49.6% |

80.7% |

An individual who moves his or her domicile to Florida, Nevada, Texas, Tennessee, or another state without any income tax or estate tax would reduce the combined income and estate tax burden to merely around 70 percent.

|

Income and Estate Taxes (Florida decedent) |

Current Law |

Biden Proposals |

|---|---|---|

|

Combined income tax |

0% (basis step-up) |

43.4%

|

|

Combined estate tax |

40% |

45.% |

|

Adjustment for reduced estate value because of income tax |

0% |

-19.5% |

|

Combined marginal income and estate taxes |

40% |

68.9% |

Although some academic commentators seem to think that Biden would not impose the income tax and the estate tax on the same amount,26 the bills that would repeal basis step-up at death do not provide a credit against the estate tax. Taxpayers should continue to follow the general post-2010 life-long tax advice to avoid dying whenever possible. Not dying provides a deferral benefit, and it is possible that a future presidential administration will change some of the tax laws and restore a basis step-up at death. Dying can increase other tax burdens such as being an inclusion event for some deferred income taxes in connection with the 2017-2018 deemed repatriation income.27 Death may also have nontax consequences.

A decedent’s estate may experience liquidity issues in paying both the income tax and the estate tax, which may encourage the purchase of life insurance policies and other tax-efficient means to pay or avoid the combined tax burden. Biden’s tax reform proposals so far have not mentioned a need for the $180 billion of federal revenues that could be raised from a repeal of the tax-free treatment of life insurance inside build-up and the tax exclusions for certain life insurance proceeds.28 A potentially less expensive way to save on the taxes is to bequest the assets to one’s spouse. Taxpayers may also consider gifts made during their lifetime and use the proposed $100,000 annual gain exclusion for gifts in conjunction with the gift tax’s $15,000 annual exclusion.

A gift, sale, or other transaction with a grantor trust continues to be ignored for federal income tax purposes29 until the trust becomes a non-grantor trust, such as upon the grantor’s death. Taxpayers may be able to achieve some estate tax savings by using grantor-retained annuity trusts. Although grantor-retained annuity trust tax advice can sometimes be expensive when it is based on a proportionate share of the tax savings achieved by the advice, taxpayers may be able to find more affordable options for legitimate advice on trust and estate planning.

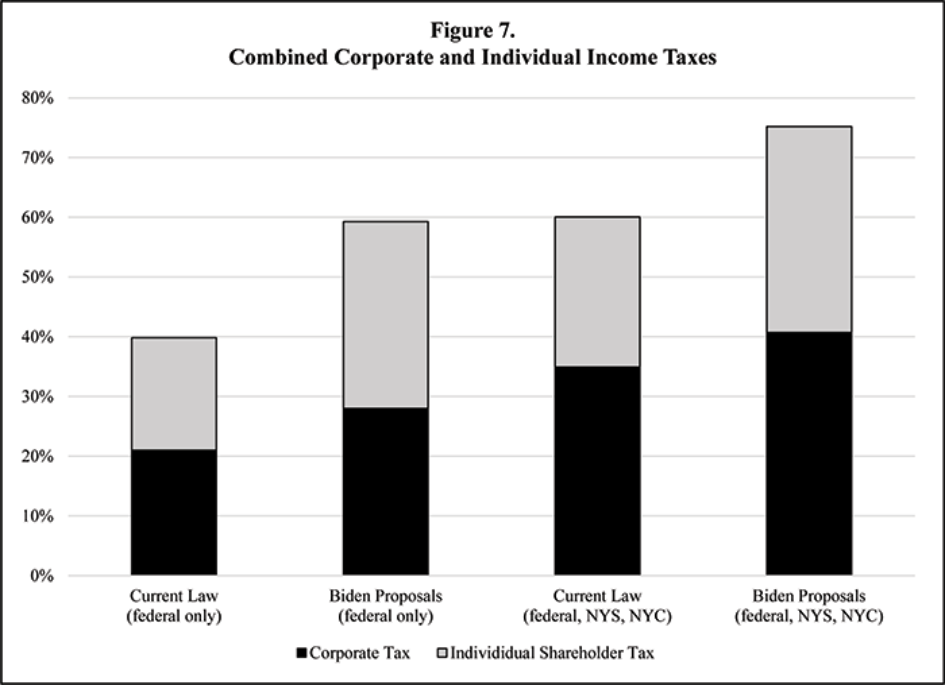

Before the TCJA, the highest federal corporate income tax rate was 35 percent, or 23.8 percent for a timber company’s timber-related capital gains.30 The TCJA reduced the federal corporate income tax rate to 21 percent beginning in 2018. If shareholder-level federal taxation is considered, the TCJA reduced the combined tax burden for corporate income from 50.5 percent to 39.8 percent.

Biden and Treasury have proposed increasing the federal corporate income tax rate to 28 percent. It is unclear whether a special lower federal income tax rate would be restored for a corporation’s timber-related capital gains.

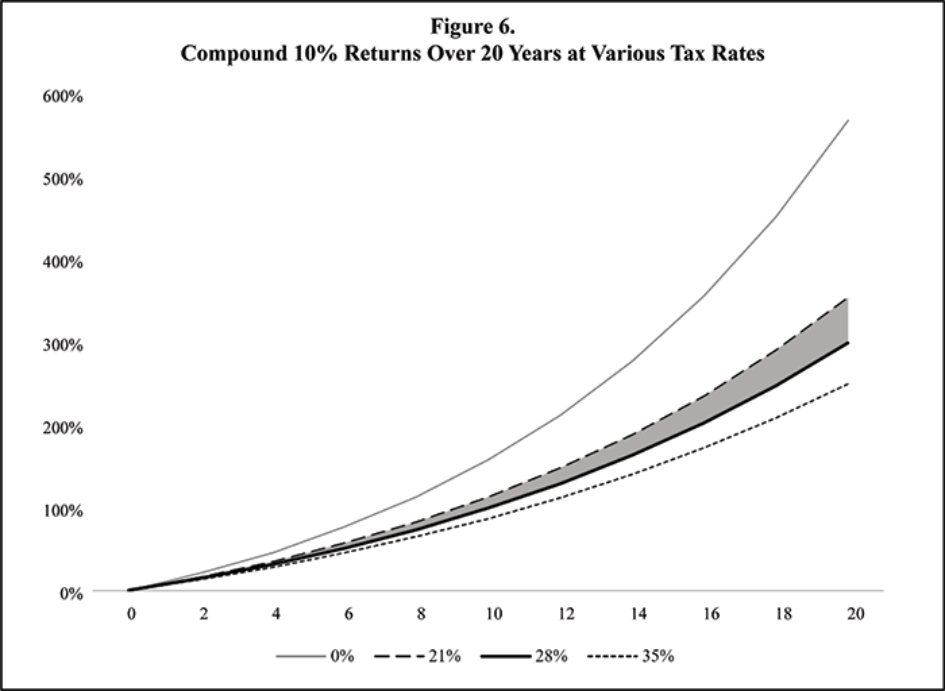

The 28 percent federal corporate income tax rate may have an adverse compounded effect on corporations’ economic returns over time and may discourage investments in research and development and other expenditures. For an investment that over 20 years has a normal 10 percent rate of annual return,31 a 28 percent tax rate creates a return gap of over 50 percent when compared with a 21 percent tax rate as shown in Figure 6. Investments with lower risk-adjusted rates of return may be canceled altogether.

The general view of many tax policy experts is that an optimal tax code has low tax rates and a broad base, which was effectuated by the TCJA and its limitations on interest deductions and use of net operating losses. A broader base with lower tax rates is sometimes followed by higher tax rates on the same broader base, which can be described in a simple three-step process:

The combined marginal federal income tax burden for corporate income is increased to 59.2 percent when the 43.4 percent shareholder-level tax on capital gains or dividend income is considered. (See Table 12.)

|

|

Current Law |

Biden Proposals |

|---|---|---|

|

Corporate income tax (federal only) |

21% |

28% |

|

Individual long-term capital gain or qualified dividend tax (federal only) |

23.8% |

43.4% |

|

Adjustment for reduced gain or dividend because of corporate income tax |

-5% |

-12.2% |

|

Combined marginal corporate and individual tax |

39.8% |

59.2% |

Like their individual counterparts, corporations may consider accelerating their income and deferring their deductions to subject more income to the currently lower tax rates. Both corporations and passthrough businesses may defer their 2021 R&D activities until 2022 or later, at which point the TCJA allows them to amortize their R&D costs over five years.32

Corporations and their shareholders can be subject to state and local income taxes. A corporation that is doing business in New York City is subject to New York state corporation tax, the maximum rate of which was recently increased to 7.25 percent; a Metropolitan Transportation Authority surcharge equal to around 30 percent of the state corporation tax; and a New York City business corporation tax. The 7.25 percent tax rate is generally retroactive as of January 1, 2021, but is temporary only through 2023, though temporary tax measures sometimes become permanent. The 7.25 percent tax rate is not marginal and has a cliff effect at $5 million of net income, so that all the taxpayer’s business income apportioned to New York is taxed at 7.25 percent once the cliff is exceeded.

|

|

Current Law |

Biden Proposals |

|---|---|---|

|

Federal corporate income tax |

21% |

28% |

|

New York state corporation tax |

7.3% |

7.3% |

|

MTA surcharge (approximate) |

2.2% |

2.2% |

|

New York City business corporation tax |

8.9% |

8.9% |

|

State deduction for New York City tax |

-0.6% |

-0.6% |

|

Federal deduction for state and city taxes |

-3.7% |

-4.9% |

|

Combined corporate income tax |

34.9% |

40.7% |

|

|

|

|

|

Individual long-term capital gain or qualified dividend tax |

36.5% |

58.2% |

|

Adjustment for reduced gain or dividend because of corporate income tax |

-12.5% |

-23.7% |

|

Combined marginal corporate and individual tax |

58.2% |

75.2% |

The combined marginal tax burden for corporate income is over 75 percent when the corporate taxes are combined with the 58.2 percent shareholder-level tax on capital gains or dividends income after considering state and New York City personal income taxes. (See Table 13.)

The TCJA repealed the corporate AMT and enacted the base erosion and antiabuse tax, which is effectively a corporate minimum tax on a broader taxable income base that disregards some deductible payments and other transactions with related foreign parties.33 The BEAT tax applies only to corporations with more than $500 million in annual gross receipts and engages in a certain amount of transactions with related foreign parties. For unclear reasons that do not appear related to the actual base erosion concerns, the BEAT does not allow foreign tax credits or most other federal tax credits.34

The good news for large multinational corporations is that Biden views BEAT as an “ineffective provision” that may be repealed. Even if BEAT is not repealed, Biden has not indicated any inclination to increase the BEAT rate, which is 10 percent from 2018 through 2025 and 12.5 percent beginning in 2026. Many taxpayers will be glad to find that they are paying less BEAT or zero BEAT because of the regular federal corporate income tax going up. However, the legislative sausage-making may result in a BEAT that is retained and reformed based on some proposed bills, such as by eliminating the 3 percent base erosion percentage threshold, counting some costs of goods sold as base erosion payments, and lowering the $500 million gross receipts threshold to $100 million or $25 million.35

Biden has proposed a 15 percent minimum tax on the book income of corporations that annually receive more than $100 million of this income, which is presumably the corporation’s income on an applicable financial statement as reported for generally accepted accounting principles or likely international financial reporting standards purposes. Biden may have been encouraged by the increasing use of GAAP and IFRS accounting for other tax purposes. Substantially all qualified Opportunity Zone tax practitioners are familiar with using Accounting Standards Codification 842, as added by Accounting Standards Update 2016-02, to value leases starting in 2019.36

In contrast to earlier minimum tax proposals by other presidential candidates, Biden’s 15 percent minimum tax allows NOL carryovers and FTCs. The FTCs would presumably be subject to the book tax equivalent of the section 904 FTC basket limitation, with FTCs limited to the book income tax on the same category of book income (general, passive, GILTI, or foreign branch book income) or a simple country-by-country approach. The book income tax’s excess FTCs in each category would then have carryovers subject to book analogues of the section 904(f) overall foreign loss rules, the section 904(g) overall domestic loss rules, and the section 904(f)(5) separate limitation loss rules.

Like BEAT, Biden’s book income tax was initially not reduced by other federal tax credits. The tax initially applied to corporations with over $100 million of book income. More recently, and apparently in response to feedback from some business sectors, Treasury has proposed that the 15 percent minimum tax apply only to corporations with more than $2 billion of book income each year and that the tax can be reduced by renewable energy tax credits and other general business credits.37 It is unclear if the tax applies only to the book income in excess of $2 billion, or whether the $2 billion threshold has a cliff effect.

The exact contours of the 15 percent minimum tax remain to be determined, but the tax seems to be inspired by the 1987-1989 corporate AMT adjustment of business untaxed reported profits (BURP) that was invented by a Yale Law School professor. Somewhat surprisingly for an idea that originated from an Ivy League institution, BURP turned out to be complex and difficult to implement.38 BURP was replaced by the simpler adjusted current earnings AMT adjustment that was more easily understood and handled by corporate tax departments in 1990 through 2017.39 Treasury seems to have learned some lessons from 1980s BURP and is harnessing the more practical expertise of law professors outside the Ivy League for the new book income tax.

Taxpayers that like to view their glasses as 28 percent full should be happy to know Biden’s proposals would increase the value of NOL carryovers. Each dollar of used NOL deduction would save 28 cents of federal income tax — instead of 21 cents — after the federal corporate income tax rate increases to 28 percent. A similar valuation increase applies to a lesser extent to individual NOL carryovers. The increased valuation of NOL carryovers after Biden’s tax reform may be considered income for financial reporting purposes, which would presumably be subject to the 15 percent minimum tax on book income. Mergers and acquisitions transactions may be more desirable for farsighted taxpayers to obtain more NOLs and other tax attributes, while they are still cheap at around 21 cents per dollar, and use them in later years for 28 cents per dollar, subject to applicable limitations on attribute use under sections 269, 381, 382, 383, and 384.

Tax advice on how to accelerate deductions and defer income has been prevalent recently — first in late 2017, when the TCJA reduced federal income tax rates beginning with the following tax year, and again in late 2020, when the CARES Act allowed a limited opportunity to carry back NOLs generated in 2020 (or in 2021 for fiscal-year taxpayers). Tax advice on how to defer deductions and accelerate income may become more popular when tax rates are expected to increase.

Some taxpayers in recent years have converted from passthrough entity structures to domestic C corporations. Given that corporate tax rates could be made materially higher than passthrough entity tax rates, they might experience second thoughts and regrettable difficulties in converting back to passthrough entities.

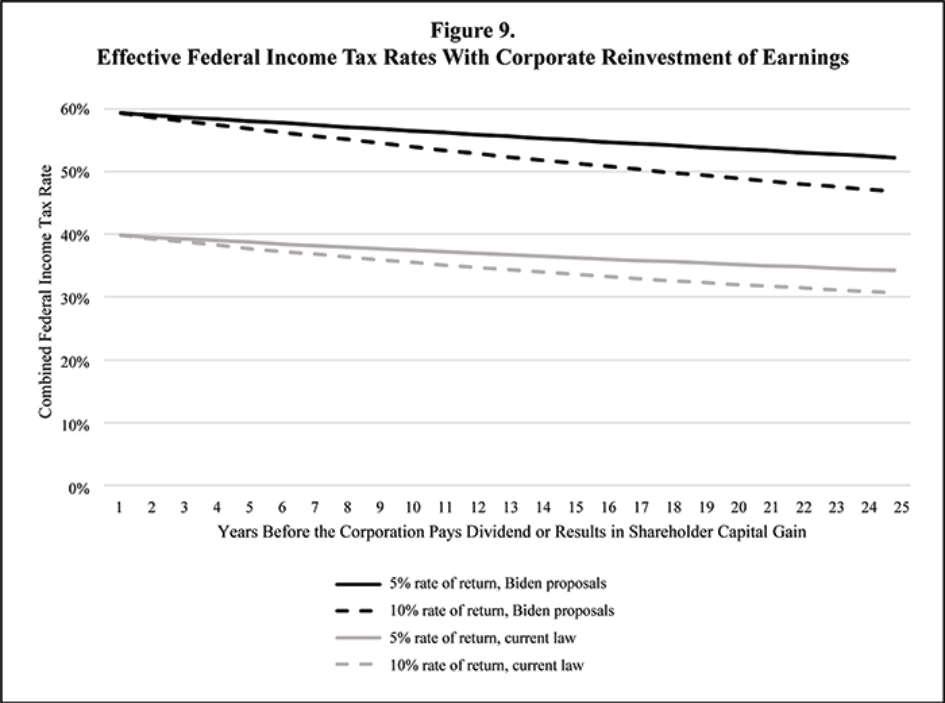

Even if domestic C corporations do not immediately distribute their income and instead reinvest their earnings at the corporate level, the benefits of deferring the shareholder-level income taxes may not be particularly significant even after considering the time value of money. A domestic C corporation would need a high rate of return on its investments for several decades before the effective combined federal income tax rate is close to the 43.4 percent rate for passthrough income, as shown in Figure 9.

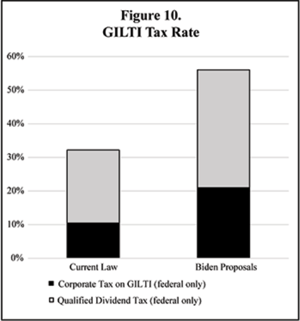

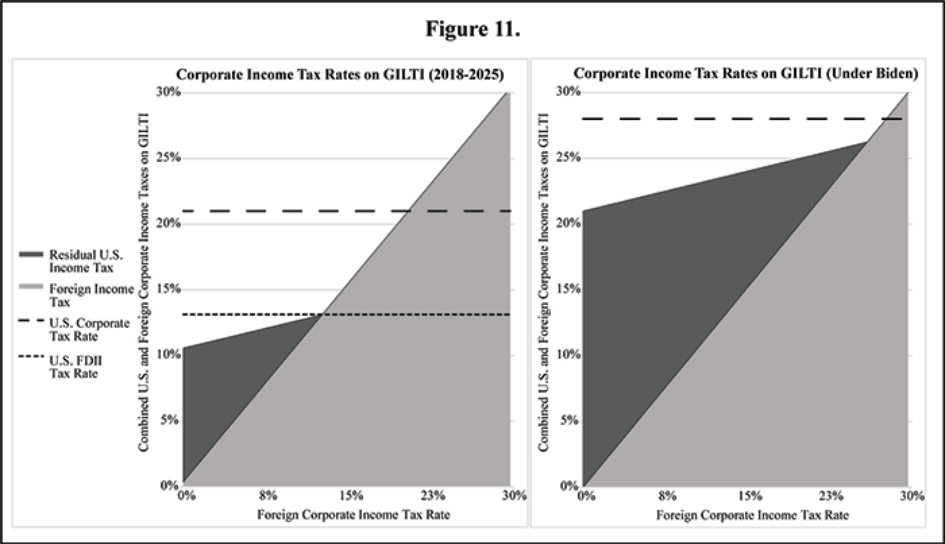

The TCJA enacted the global intangible low-taxed income regime, which generally imposes a 10.5 percent effective federal income tax rate from 2018 through 2025 on some foreign earnings of a domestic corporation’s foreign subsidiaries.40 The effective federal corporate income tax rate on GILTI increases to 13.125 percent in 2026. The U.S. tax on GILTI inclusions is reduced by 80 percent of any FTCs for foreign income taxes imposed on the foreign earnings.41 GILTI’s purpose is to impose a minimum amount of U.S. and foreign income tax on some intangible income.

For the GILTI regime to apply to intangible income and not to tangible income, a taxpayer’s GILTI inclusions are generally reduced by an imputed return of 10 percent on its foreign subsidiaries’ depreciable tangible assets (qualified business asset investment).42 Income from foreign tangible assets are viewed as less prone to offshoring, particularly given that a U.S.-owned foreign factory is more likely to be replaced by a foreign-owned foreign factory than a U.S.-owned U.S. factory. The tax-free treatment of foreign tangible income has been criticized by academic commentators,43 Biden, Treasury,44 and Senate Democrats,45 who may not fully appreciate that the purpose of the GILTI regime is to tax foreign intangible income and to avoid taxing foreign income derived from foreign tangible assets. The repeal of the QBAI exemption for tangible income may require GILTI to be renamed “global international low-taxed income” and cause some consternation at Treasury’s Department of Redundancy Department.

Biden has proposed doubling the effective GILTI federal tax rate to 21 percent. Under current law, GILTI’s 10.5 percent effective federal tax rate is achieved by using a 50 percent section 250 deduction. With Biden’s 28 percent federal income tax rate, a reduced 25 percent section 250 deduction is sufficient for GILTI to have an effective tax rate of 21 percent. The combined federal tax burden on GILTI increases from 32 percent to 55 percent when shareholder-level taxes are considered.

A controlled foreign corporation’s shareholder with GILTI subject to 26.25 percent foreign income tax would be allowed 80 percent of those foreign income taxes as FTCs. The 21 percent FTCs would entirely offset the 21 percent U.S. income tax on the GILTI inclusions. The GILTI foreign income tax break-even point is therefore 26.25 percent, above which there is no residual U.S. income tax, assuming that no expenses are allocated and apportioned to the GILTI inclusions. The break-even point is currently 13.125 percent.

|

GILTI |

Current Law |

Biden Proposals |

|---|---|---|

|

Corporate income tax on GILTI (federal only) |

10.5% |

21% |

|

Individual long-term capital gain or qualified dividend tax (federal only) |

23.8% |

43.4% |

|

Adjustment for reduced gain or dividend because of corporate income tax |

-2.5% |

-9.1% |

|

Combined corporate and individual tax |

31.8% |

55.3% |

GILTI affects not only U.S.-based multinationals but also individual U.S. shareholders of foreign corporations, if they own (directly or constructively) 10 percent or more of the stock of a CFC. The individual shareholder is generally taxed on GILTI at full ordinary income rates and without any indirect FTCs, which is worse than their corporate shareholder counterpart, who can benefit from the section 250 deduction and some indirect FTCs.

Ever since the Revenue Act of 1962, the popular section 962 election has allowed the individual taxpayer to elect to be subject to corporate income tax rates on subpart F inclusions (since 1962) and GILTI inclusions (in 2018 and later). The election reduces the federal income tax rate on the inclusions and allows the U.S. tax to be reduced by indirect FTCs from the CFC’s foreign income taxes. The downside of the election is that part or all of the CFC’s actual distributions to the electing individual U.S. shareholder are taxed as dividends.

The section 962 election results in a slightly higher overall tax burden on GILTI compared with using a real domestic C corporation, because the section 1411 Medicare tax is higher. Although section 962(d) provides that some CFC distributions to the section-962-electing individual shareholder are tax-free previously taxed income distributions, the section 1411 tax does not follow the PTI rules and is typically imposed on PTI amounts.46 (See Table 15.)

|

|

Current Law |

Biden Proposals |

|---|---|---|

|

Corporate income tax on GILTI (federal only) |

10.5% |

21% |

|

Individual long-term capital gain or qualified dividend tax (federal only) |

23.8% |

43.4% |

|

Adjustment for reduced gain or dividend because of corporate income tax |

-2.1% |

-8.3% |

|

Combined corporate and individual tax for individual with section 962 election |

32.2% |

56.1% |

The landmark case of Smith v. Commissioner47 confirmed that the CFC’s distributions to the electing individual U.S. shareholder are taxed as dividends from a foreign corporation, instead of a dividend from a deemed domestic corporation. A foreign corporation can pay qualified dividends if it is organized in some treaty countries or if it is publicly traded in the United States.48 For a CFC in a non-treaty country such as the Hong Kong CFC in Smith, the combined tax burden is higher under current law but would be equalized with the Biden proposals that increase qualified dividend tax rates to ordinary income tax rates.

|

CFC That Does Not Pay Qualified Dividends |

Current Law |

Biden Proposals |

|---|---|---|

|

Corporate income tax on GILTI (federal only) |

10.5% |

21% |

|

Individual ordinary dividend tax (federal only) |

40.8% |

43.4% |

|

Adjustment for reduced gain or dividend because of corporate income tax |

-3.9% |

-8.3% |

|

Combined corporate and individual tax for individual with section 962 election |

47.4% |

56.1% |

GILTI does not include income excluded from subpart F income by reason of the section 954(b)(4) high-tax exclusion for subpart F income subject to foreign income tax rates greater than 90 percent of the federal corporate income tax rate.49 Treasury and the IRS were able to think outside the statutory box and permitted taxpayers to exclude all foreign income subject to foreign income tax rates greater than 90 percent of the federal corporate income tax rate.50 The GILTI high-tax exclusion is better for taxpayers that may not be able to fully use their FTCs, such as because of allocation and apportionment issues; BEAT; or status as an individual who does not make a section 962 election, a REIT, or a regulated investment company. The GILTI high-tax exclusion is also preferred by taxpayers that do not wish to use their NOL carryovers, passive activity loss carryovers, or other tax attributes against GILTI inclusions.

Under the current 21 percent federal corporate income tax rate, the subpart F and GILTI high-tax exclusions apply to income subject to more than 18.9 percent foreign income tax. If the federal corporate income tax rate is increased to 28 percent, the subpart F and GILTI high-tax exclusions would apply only to income subject to more than 25.2 percent foreign income tax (25.2 percent is 90 percent of 28 percent). The subpart F and GILTI high-tax exclusions would therefore cease to apply to some income from countries where the tax rate is between 18.9 percent and 25.2 percent, including the following OECD countries based on their average tax burdens:

The 25.2 percent foreign income tax rate threshold for the high-tax exclusions is below the 26.25 percent GILTI break-even point for foreign income tax rate with full use of FTCs, which can create some different incentives compared with current law under which the 18.9 percent threshold for the high-tax exclusions is above the 13.125 percent GILTI break-even point.

The GILTI high-tax exclusion is unpopular among some academic commentators. There have been legislative proposals to repeal the GILTI and subpart F high-tax exclusions and to limit all FTCs on a country-by-country system.51

The TCJA’s intent was to move the U.S. international tax regime from a worldwide taxation system (with deferral) to a territorial taxation system. The proposed GILTI reforms would move the United States closer to a worldwide taxation system (without deferral), as favored by some academic commentators. Some domestic companies may view the United States as less competitive compared with its fully territorial peers and may be tempted to become a foreign company to avoid U.S. income tax on their foreign earnings. The Biden administration may respond by using the section 7874 anti-inversion rules, which may or may not have been successful in preventing inversions in the years since their enactment by the American Jobs Creation Act of 2004.

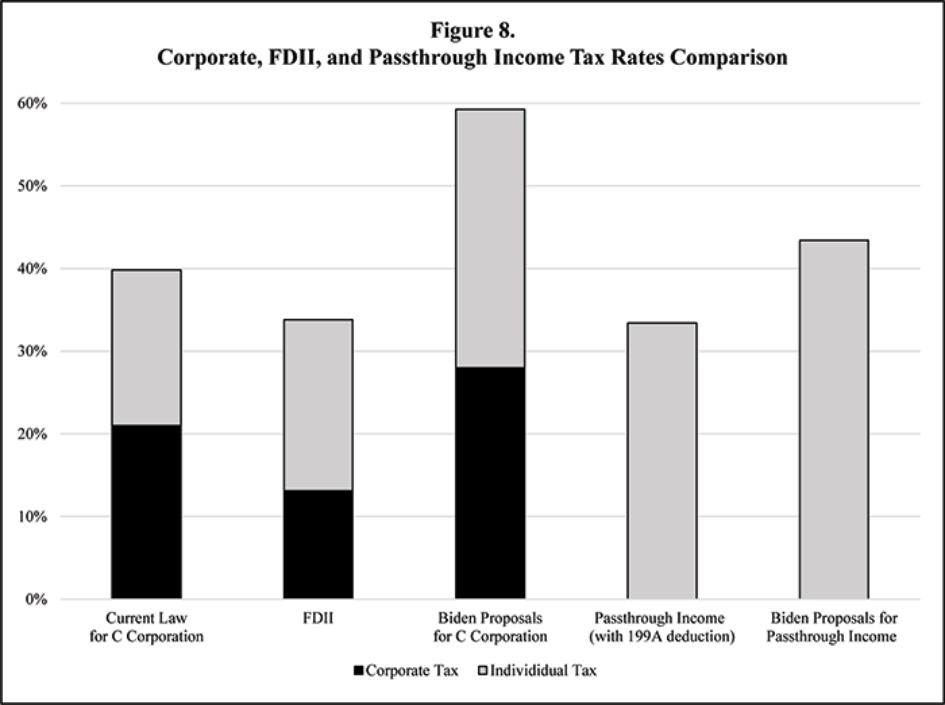

As the carrot to the GILTI stick, the TCJA enacted the section 250 deduction to reduce the effective federal income tax rate for a domestic corporation’s foreign-derived intangible income, such as income from export sales and licensing royalties paid by foreign parties. The effective federal tax rate for FDII is 13.125 percent from 2018 through 2025, and 16.406 percent beginning in 2026.

Biden has proposed to repeal FDII, which is labeled as giving “corporations a tax break for shifting assets abroad and is ineffective at encouraging corporations to invest in R&D.” It is possible that Biden would either repeal FDII entirely or cause the FDII effective tax rate to equal the GILTI foreign income tax rate break-even point of 26.25 percent.

Some tax advisors have suggested that foreign companies set up domestic C corporations to generate sales subject to U.S. corporate tax but reduced by the FDII deduction.52 Any such major business decision would take into account many factors, including (i) state income taxes, such as Florida’s corporate income tax of up to 5.5 percent (temporarily lower in 2019-2021); (ii) the probability-weighed and discounted likelihood of FDII repeal or reduction; and (iii) the built-in gain tax liability and other difficulties if the domestic C corporation were later unwound and liquidated to bring its assets back offshore.

|

|

Current Law |

Biden Proposal |

|---|---|---|

|

Effective FDII federal corporate income tax rate with 37.5% section 250 deduction (2018 through 2025) |

13.125% |

17.5% |

|

Effective FDII federal corporate income tax rate with 21.875% section 250 deduction (2026 and later) |

16.406% |

21.875% |

|

Effective FDII federal corporate income tax rate with 6.25% section 250 deduction (equivalent to GILTI break-even point) |

|

26.25% |

|

Effective FDII federal corporate income tax rate with FDII repeal |

|

28% |

Foreign individuals with income effectively connected with the conduct of a U.S. trade or business (ECI) are subject to graduated rates of federal income tax like U.S. individuals of up to 37 percent, and up to 39.6 percent under Biden’s proposals.53 Nonresident aliens are not subject to the section 1411 Medicare tax.54

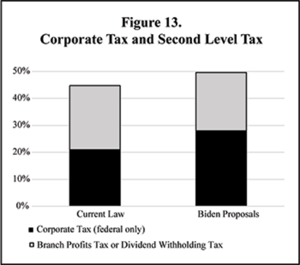

Foreign corporations with ECI are generally subject to both the federal corporate income tax and the branch profits tax of up to 30 percent.55 When the TCJA reduced the federal corporate income tax rate from 35 percent to 21 percent, the combined tax burden, including the branch profits tax, was reduced from 54.5 percent to 44.7 percent.

The post-TCJA quip of “45 is the new 55” becomes “50 is the new 55” if Biden increases the federal corporate income tax rate from 21 percent to 28 percent. The combined tax burden rises to 49.6 percent when the branch profits tax is included. A similar combined 49.6 percent tax burden applies to a domestic C corporation that pays 28 percent federal corporate income tax and a 30 percent dividend withholding tax on a dividend paid to a foreign shareholder in a non-treaty country.

|

|

Current Law |

Biden Proposals |

|---|---|---|

|

Corporate income tax rate (federal only) |

21% |

28% |

|

Branch profits tax |

30% |

30% |

|

Reduction in branch profits tax because of corporate income tax |

-6.3% |

-8.4% |

|

Combined income tax rate for foreign corporation |

44.7% |

49.6% |

Foreign corporations are also subject to state and local income taxes like their domestic corporate counterparts. Some foreign corporations may avoid U.S. federal income tax on their ECI under income tax treaties that require a permanent establishment for the imposition of U.S. federal income tax on ECI. U.S. states and localities are not bound by U.S. income tax treaties with foreign countries and may have differing ideas about imposing taxes on foreign taxpayers that derive income from a U.S. trade or business.

President Biden has made many tax proposals over the course of his campaign and presidency, including the repeal of section 1031 like-kind exchanges, restrictions on itemized deductions that may discourage home mortgage financing and charitable contributions, and incentives for renewable energy and manufacturing activities in the United States that have not yet been sent to Treasury’s Brainstorm and Review Acronym Naming Division (BRAND). But the proposed increases to individual and corporate income tax rates have drawn the most attention.

Some taxpayers may look forward to combined income and estate tax rates of 70 percent or 80 percent imposed on the assets that they own at death, which may lead to more spending on consumable goods and services instead of holding savings and investments that would be mostly handed over to the government at death. A high tax rate on a high-income taxpayer’s assets at death is economically equivalent to a delayed but refundable federal tax credit for lifetime spending. Other effects of these tax incentives may include more contributions to private foundations, acquisitions of family farms that are more likely to be exempt from the rules, and more spending on legitimate advice about trust and estate planning.

The increased federal income tax rates have many different effects on taxpayers beyond additional annual tax payments to the IRS. Some partnership and limited liability company agreements provide for tax distributions at the highest marginal tax rates, which may be increased for some partners or members. Partnerships may find themselves paying more imputed underpayments under the centralized partnership audit rules as enacted by the Bipartisan Budget Act of 2015. Higher tax rates can affect tax insurance in mergers, acquisitions, and other transactions. Some tax insurance carriers may carve out retroactive tax increases from the insurance coverage in exchange for lower premiums paid by the insured.

FOOTNOTES

1 White House, “Fact Sheet: The American Jobs Plan” (Mar. 31, 2021).

2 Id. (“The President looks forward to working with Congress, and will be putting forward additional ideas in the coming weeks for reforming our tax code so that it rewards work and not wealth, and makes sure the highest income individuals pay their fair share.”)

3 See Libin Zhang, “Marginal Income Tax Rates of the Passthrough Business Deduction,” Tax Notes, May 21, 2018, p. 1139.

4 See Treasury, “The Made in America Tax Plan” (Apr. 2021).

5 But see Notice 2020-75.

6 See Andrew Duehren, “Senate Parliamentarian Rules in Favor of Democratic Reconciliation Effort,” The Wall Street Journal, Apr. 5, 2021.

7 See Jad Chamseddine, “Democrats Threaten Next Tax Bill Over SALT Cap,” Tax Notes Today State, Mar. 31, 2021.

8 “Biden-Sanders Unity Task Force Recommendations: Combating the Climate Crisis and Pursuing Environmental Justice” (July 2020).

9 Gov. Andrew Cuomo, “Video, Audio, Photos & Rush Transcript: Governor Cuomo Presents Highlights of FY 2022 Budget to Reimagine, Rebuild and Renew New York” (Apr. 7, 2021).

12 H.R. 1068 (Carried Interest Fairness Act of 2021).

13 The TCJA also repealed the 9 percent former section 199 deduction for domestic production activities in 2018 and later, although some taxpayers were still able to claim the 9 percent deduction against the 21 percent corporate tax rate in 2018, to achieve a 19.11 percent federal corporate income tax rate in 2018, by careful use of passthrough entities and fiscal years.

14 White House, “Press Briefing by Press Secretary Jen Psaki and Secretary of Education Miguel Cardona, March 17, 2021.”

15 White House, “Press Briefing by Press Secretary Jen Psaki, Chair of the Council of Economic Advisers Cecilia Rouse, and Member of the Council of Economic Advisers Heather Boushey, March 24, 2021”; “Press Briefing by Press Secretary Jen Psaki, March 29, 2021.”

16 Sections 168(e)(3)(C)(ii), 168(i)(15).

21 Sections 164(f), 1402(a)(12).

22 See Paul Jones, “California Lawmakers Reintroduce Millionaire’s Tax,” Tax Notes Today State, Mar. 30, 2021.

23 Richard Rubin, “How Joe Biden’s Tax Plan Could Affect You,” The Wall Street Journal, Nov. 9, 2020.

24 See H.R. 2286 (Sensible Taxation and Equity Promotion Act of 2021) (Mar. 29, 2021).

25 White House Office of the Press Secretary, “Fact Sheet: A Simpler, Fairer Tax Code That Responsibly Invests in Middle Class Families” (Jan. 17, 2015).

26 Jonathan Curry, “The Sky May Not Be Falling for Estate Planners After All,” Tax Notes Federal, Feb. 22, 2021, p. 1286.

28 See Tax Expenditures, available at Treasury's website.

29 Rev. Rul. 85-13.

30 Former section 1201(b).

34 Section 59A(b)(1)(B). See New York State Bar Association Tax Section, “Report No. 1397 on Base Erosion and Anti-Abuse Tax,” at 7 (July 16, 2018) (BEAT treatment of FTCs is “difficult to understand”).

35 See, e.g., S. 725 (Stop Tax Haven Abuse Act) (Mar. 11, 2021); Corporate Tax Dodging Prevention Act.

36 See Treas. reg. section 1.1400Z2(d)-1(b)(3); American Bar Association Section of Taxation, “Re: Proposed Regulations Regarding Investments in Qualified Opportunity Funds Under Section 1400Z-2,” at 8 (Jan. 10, 2019).

37 See Treasury, “The Made in America Tax Plan” (Apr. 2021).

38 Arthur I. Gould, “The Corporate Alternative Minimum Tax: A Search for Equity Through a Maze of Complexity,” 64 Taxes 783 (1986); Sandra G. Soneff Redmond, “The Book Income Adjustment in the 1986 Tax Reform Act Corporate Minimum Tax: Has Congress Added Needless Complexity in the Name of Fairness?” 40 Sw. L.J. 1219 (1986).

39 Former section 56(g).

43 See, e.g., Andrew Velarde, “Perceived GILTI Shortcomings Focus of Senate Hearing,” Tax Notes Federal, Mar. 29, 2021, p. 2084.

44 See Treasury, supra note 37.

45 Senate Finance Committee, “Overhauling International Taxation” (Apr. 1, 2021).

46 Treas. reg. section 1.1411-10(c)(1)(i)(A)(1).

47 151 T.C. 41 (2018).

50 Treas. reg. section 1.951A-2(c)(7).

51 See, e.g., No Tax Breaks for Outsourcing Act; Senate Finance Committee, supra note 45.

52 See Steven Hadjilogiou et al., “Because of FDII, Every Global Supply Chain Should Consider a U.S. C Corporation,” Tax Notes Int’l, Mar. 29, 2021, p. 1647.

END FOOTNOTES